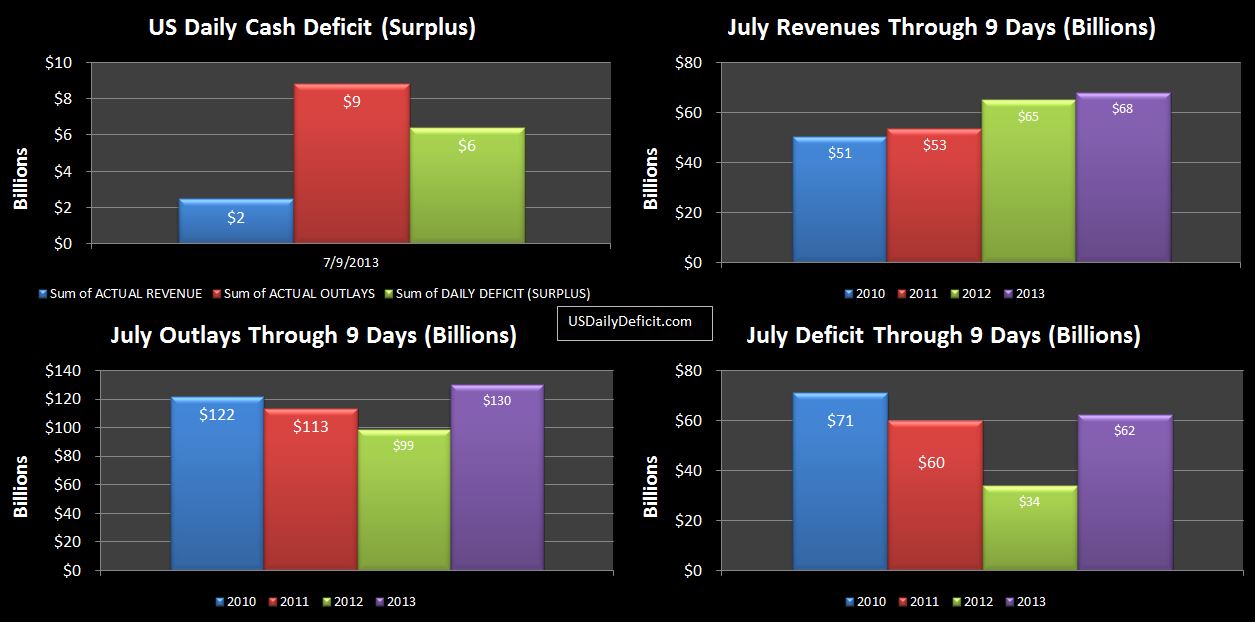

One of the first challenges I faced when I decided to use the treasury department’s “Daily Treasury Statement” was to reconcile the thing to other external data points like the debt outstanding and cash balances as well as internally reconciling the tables within it to make sure I understood the report inside and out, and furthermore, trusted it. In this quest I ended up stumbling on one thing I could not answer…the “Cash FTD(federal tax deposits)” category in table II…which makes up over 2/3 of all cash deposits never tied to table IV, which summarizes tax deposits by type, like withheld income, corporate taxes ect… It was perpetually short by a category labeled “Inter-Agency Transfers”

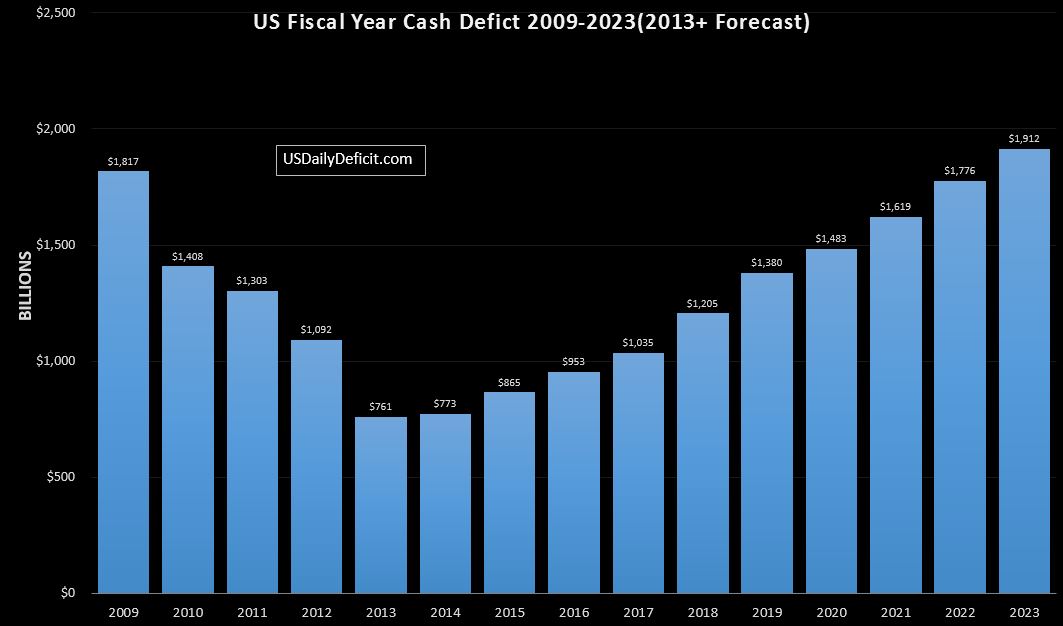

It took some back and forth, but the good folks at Treasury provided the clues I needed. This imbalance..$82B over FY 2012 is due primarily to the affect of FICA taxes and Income taxes withheld from the paychecks of federal employees.

Before we look at that, lets start by looking at a regular employee of a fortune 500 company. Say the person has an annual salary of $100k, $25k of which is withheld from the paycheck and submitted to the federal government by the company. This $25k (plus another $7650 for FICA) shows up on the DTS as cash received in the “CASH FTD” category.

Now….let’s use the same example, but this time the employee works for the federal government. Each year…the government sends the employee his $75k of cash….but what to do with the $25k of taxes withheld? Transfering $ from one bank account to another has no net affect on cash in this scenario…unlike when it was submitted by the fortune 500 company. The plug is “Inter-Agency Transfer…essentially an intercompany elimination. This is why we have the $82 difference. That $25k of taxes “paid” by the employee show up in the official tax receipts number…even though no marginal cash is ever received…it just gets shuttled around from one federal bank account to the next…netting out to zero. 82B per year!!

Looking at this from another angle…say the federal government has revenues of exactly $1T, and the economy is perfectly stable…no change in employment, no raises ect…everything is constant. Then, the government decides to hire our employee for $100k per year. When all is said and done…government revenues have stayed exactly the same, even though income is up $100k, and reported income taxes are up $25k. Contrast that to if the employee was hired by a company…then government revenues would have increased by $25k+. Isn’t that something? The federal government could go out and hire 5M people….and it would have exactly no direct increase in cash inflows. Or…you could fire all of the current employees…and cash inflows would not drop a penny.

So what is going on here? Essentially, the cost associated with federal employees income and payroll taxes, and the revenue they represent, net to zero. The affect is…that the federal government can essentially hire identical employees, yet effectively pay quite a bit less than a company would bringing up an interesting point….that in the end, consumers pay all taxes. In order to get $75k of cash to the employee, a company has to pay $100k because Uncle Sam want’s his “rent”….as if he owned you. That cost…is pushed all the way through the value chain and ultimately ends up on the retail shelf, raising the cost of everything…probably by a factor of nearly 2 when all is said and done. Ponder on that for a while….you can raise taxes on whoever or whatever you want in the short run, but in the long run, the economy re-adjusts back to equilibrium…with higher prices for everything as the plug.

So…to answer our question…while government employees end up with the same after tax pay as a corporate employee with similar gross pay does, their income taxes more or less manifest themselves as a discount to the federal government rather than cash receipts or actual revenues. I think that the reality is…not only do Federal employees not pay income/payroll taxes…none of us as individuals do. Instead…our employers essentially pay a consumption tax on our labor pushing the cost of a $75k per year employee up over $100k. If there were no income/payroll taxes, our employee’s take home salary would still be around $75k…but it would go a lot further because the price of everything would be 25-50% lower. Instead….consumers simply pay more. Our employer pays over $100k for a $75k employee just like at the grocery store, you pay $2, for a $1 loaf of bread.