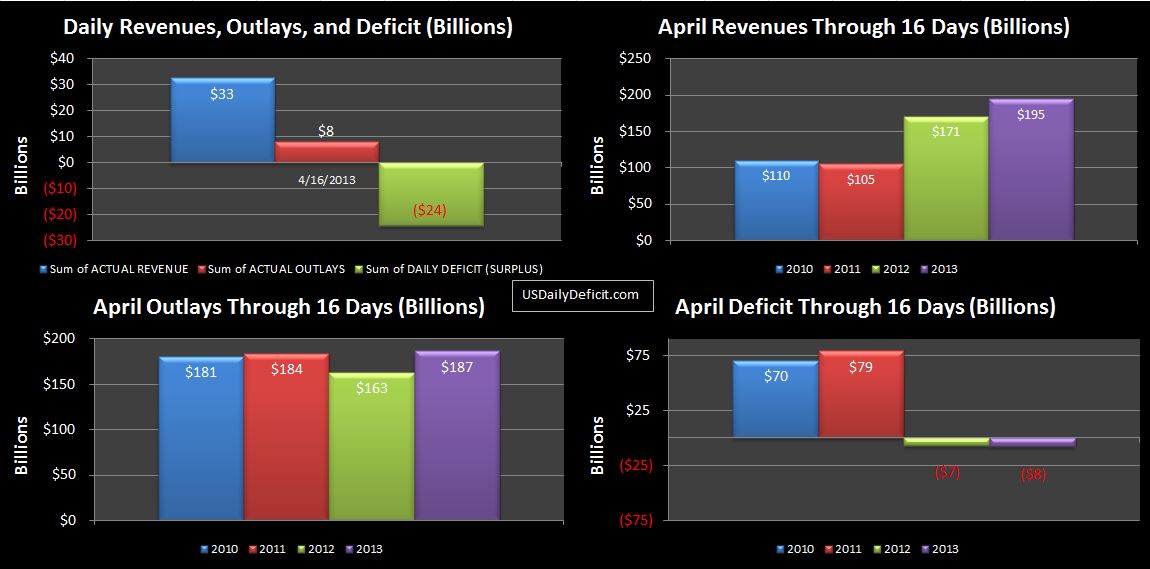

The US Daily Cash Surplus for 4/16/2013 was $24.4B pushing April 2013 to a surplus of $8B, now $1B ahead of last year through the same number of business days. Strong revenues is the big story here with the haul over the last two days exceeding the same period last year by $19B. Looking at the month to date, net revenue is up $24B, good for a 14% increase. Corporate tax deposits are up 27%, and tax deposits not withheld are up 25%.