The July 2013 deficit at $90B, was $8B higher than last July’s $82B deficit. It’s not a huge miss, but a deep dive into the details will tell a little bit different story.

Revenues:

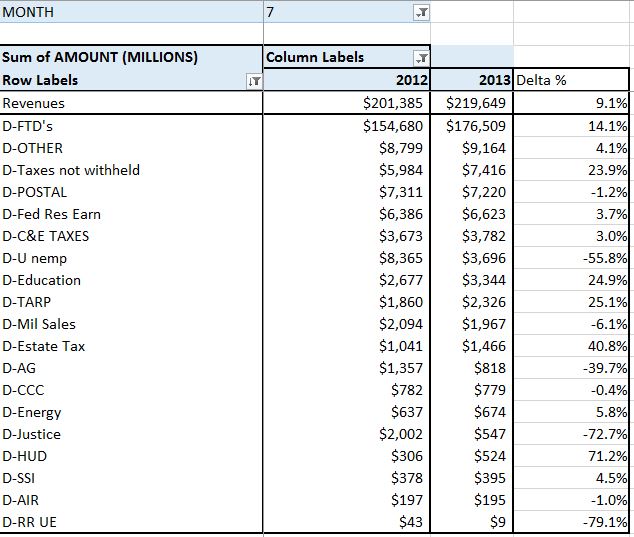

Net cash revenues came in at $220B compared to $201B last year for a 9% YOY growth. Without a doubt, it’s a good number, but it is a material step down from the 15%+ we averaged over the Jan-April period. The chart below shows the YOY revenues for a selection of the larger cash revenue categories.

The top line has total cash revenues. Most of the story can be seen in the next line…Federal Tax Deposits (FTD’s). Up $22B, 14%. It was aided by an extra day, but no matter how you look at it, this is a good solid number. Taxes not withheld were also up…this time 24%, but this is a slow month, and that only netted $1.5B. The only other material change worth noting was the 56% reduction ($4.7B) in unemployment deposits from the states. Believe it or not, this program is kinda sorta actually run like an insurance program, so I can only guess that perhaps premiums have decreased as we ease ourselves away from the Great Recession?? In any case, this category is usually good for $50-60B per year of cash revenues that I had projected to grow at 5%…I may need to revisit that assumption. But bottom line on revenues…up by a healthy amount, just not as much as before. It wouldn’t shock me one bit if we saw this ~10% growth continue through the rest of the year…It’s what comes in January 2014 that we should be concerned about.

Outlays:

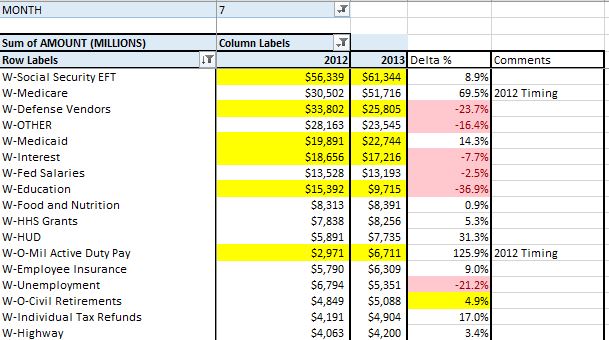

Cash Outlays were up $27B YOY from last year’s $283B to $310B in July 2013. However….last July was about $35B light due to payments due 7/1 going out early because of the weekend. If we adjust for this, we actually see an $8B overall reduction.

Catch up (June/July 2018 Cash Deficit)