Will we never learn? Without a lot of fanfare, the debt limit was reinstated on 3/15/2017 at $19.809T and Treasury instituted the infamous “Extraordinary Measures” (EM) to circumvent the law and give our politicians more time to make fools of themselves.

Extraordinary Measures??

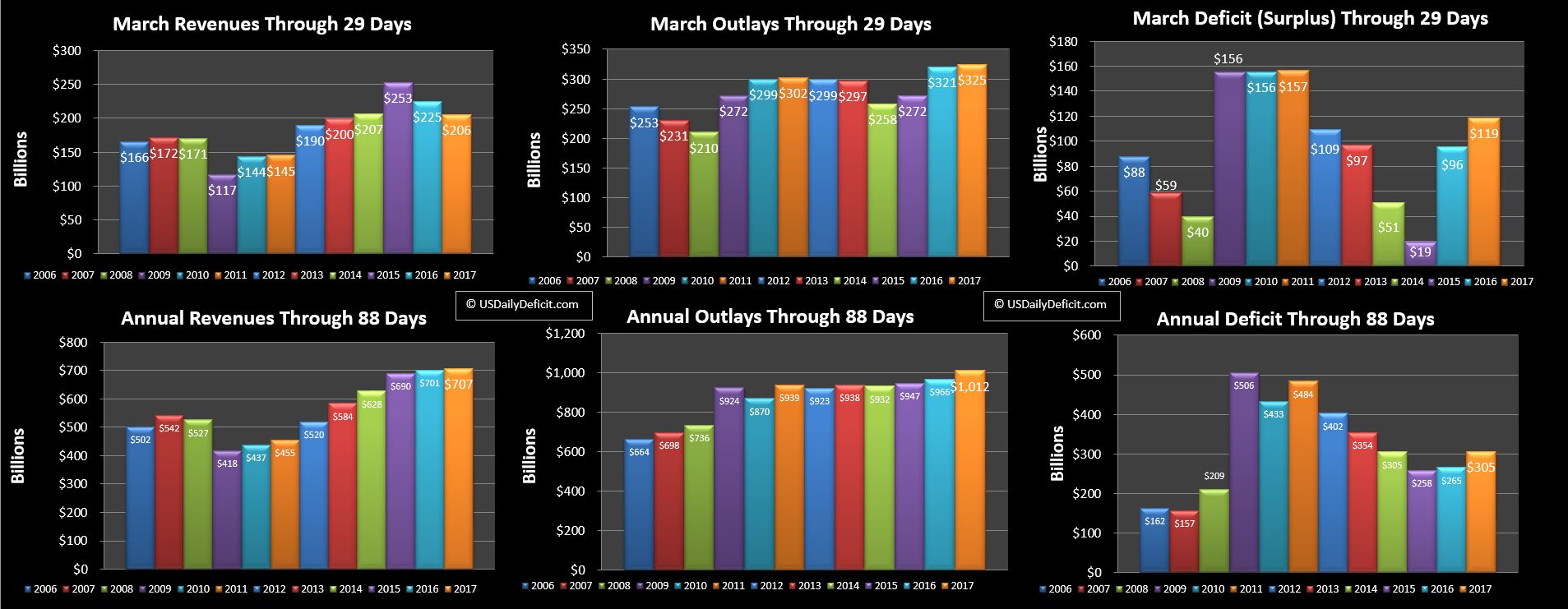

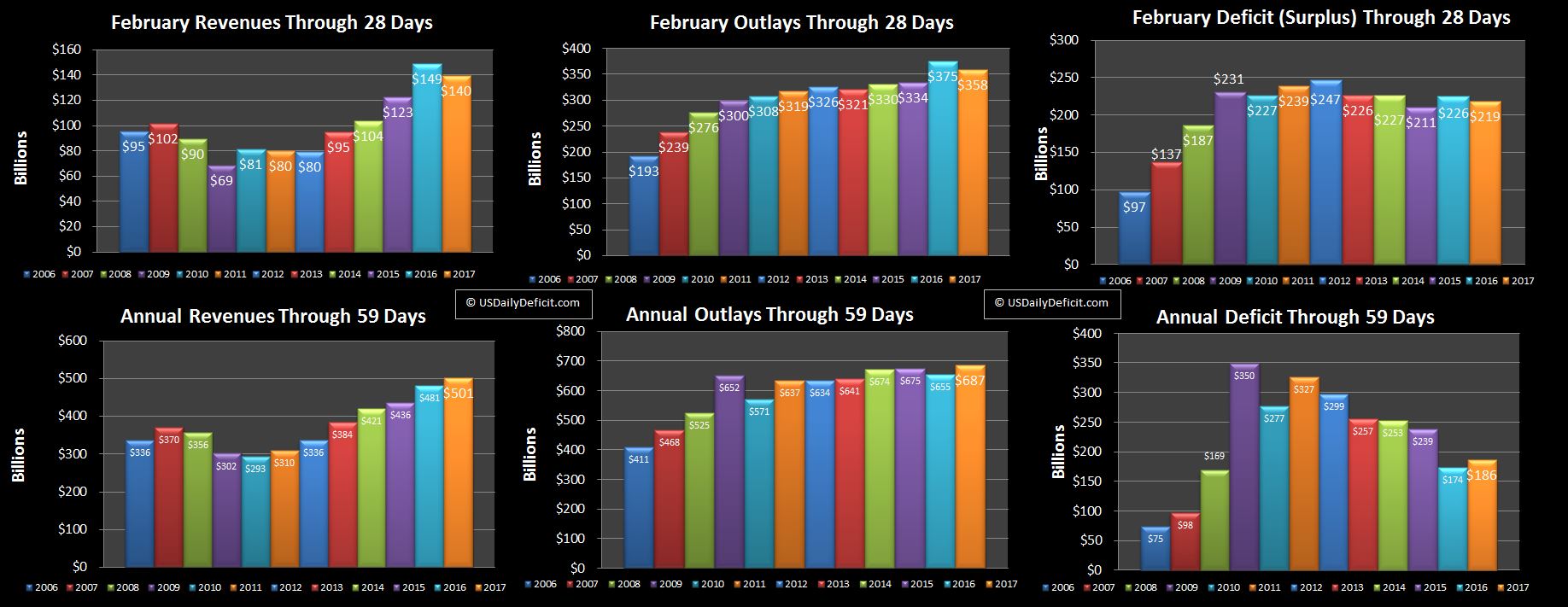

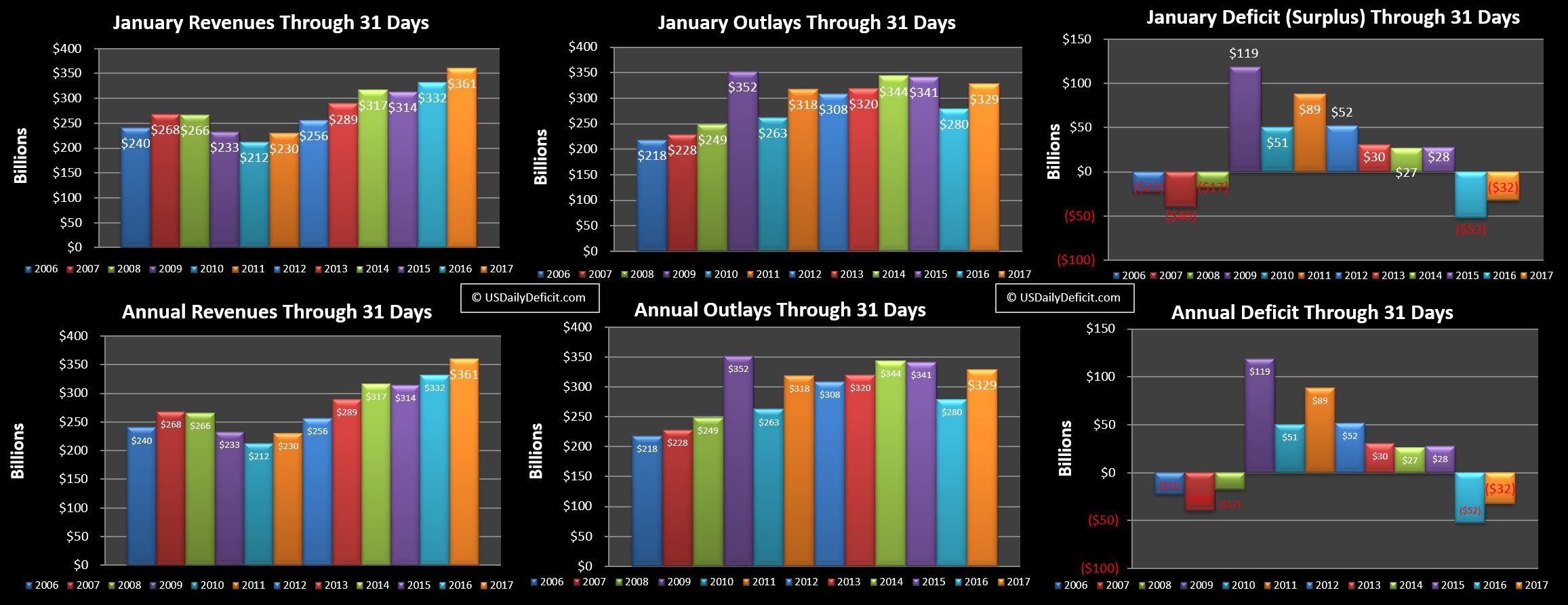

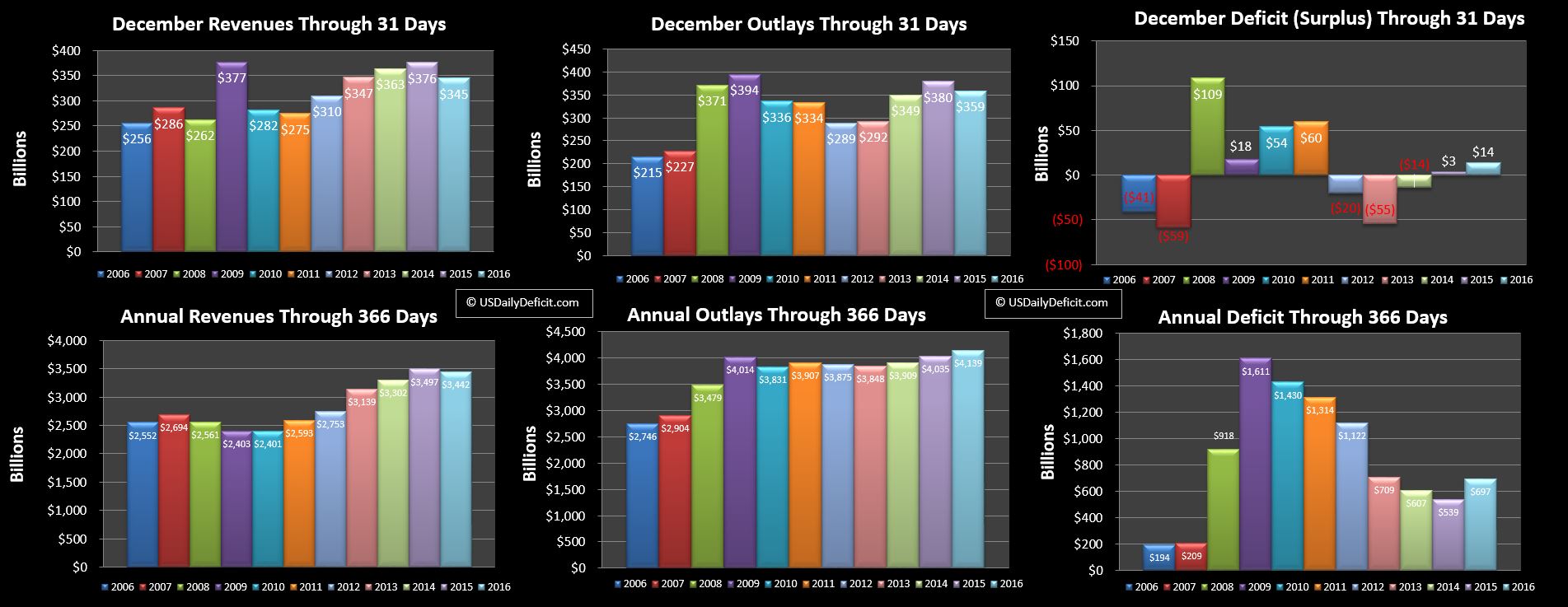

First off…what are Extraordinary Measures? For me, they are a huge pain in the rear. You see, calculating the “cash” deficit is actually a very simple exercise…we look at the change in cash balance, and adjust it for the change in debt…and voila!! So for example on 3/3/2017 the cash balance dropped by $22.080B and the debt decreased by $235M. Add them together and we get a daily cash deficit of $21.845B. Of course you can add up all of the revenue line items and subtract out the outlays….and come up with the exact same answer. Of course…I actually do that as well, but you don’t need all of that complexity to calculate the cash deficit. In any case, EM nukes my process, and while I can back into a decent educated guess, unfortunately I won’t have an actual number until these shenanigans are over. The margin of error is ~$5B a month, which actually isn’t bad, but still enough to drive the accountant in me a little nuts.

The mechanism for EM is actually quite simple…they take some parts of the debt…I can’t remember specifically off of the top of my head but things like federal retirement funds…and simply pretend thy don’t exist(a little at a time). This simple move lowers the official debt outstanding, allowing them to continue to issue new debt. When the debt limit is ultimately increased, they just pull all of the EM debt they were pretending didn’t exist back onto the balance sheet resulting in a huge one day increase. Last time we played this game back in late 2015 the result was a $339B increase, so it seems reasonable to think they can squeeze about $350B of EM this time.

How Long Do We Have?

Last time around the timing of the debt limit was the same if I recall…debt limit reinstated 3/15/2015, and EM used to get us all the way to the resolution in early November…so over 7 months. As I stated back then…the middle of March is just about the best possible time for a debt limit standoff because the huge outflows of tax refunds are pretty much behind you, and you are just a month removed from a huge inflows in April which as of late have been running in the ballpark of a $200B surplus. With an April surplus and $350B of EM…and getting to October/November again seems like a pretty solid bet.

Cheney was right…Deficits Don’t Matter(Anymore)

Here is what I know…the US debt/deficit is a massive problem. It will blow up, and there will be a lot of pain….maybe worse. This will happen…I am 100% certain of it. The window to fix it has now closed….I’m not sure it was ever really open. Could be this year…could be 20 years from now…but it will happen. But since it’s going to happen, I’ve stopped worrying about it. Why should republicans who don’t care about the deficit and democrats who don’t care about the deficit fight over some measily $15B here or there…when obviously the American people don’t care about the deficit either? Just hours ago….the republicans plan the shoot down the much hated and relatively new entitlement(ACA…AKA Obamacare) went down in flames despite Republicans having the presidency and majorities in congress. This is the system that is going to fix $20T in debt…growing at ~1T per year indefinitely? Hah!!

My thoughts on the matter have changed a lot over the last few years as I have accepted this reality. Rather than worrying about it…we should just enjoy it as long as we can. As long as there are still suckers around willing to buy “risk free” US debt…let them!! So this is my advice to Trump and the Republicans….stop pretending to care about the debt…we don’t believe you…you aren’t impressing anyone, and honestly nobody even cares anymore. So forget about it and go big on things people do care about. Tax cuts, jobs, infrastructure,trade, immigration….heck maybe break up the medical industry that seems more interested in financially screwing us over every time we walk into an office or hospital than actually improving health.

So pass the silly debt limit increase or better yet just get rid of it….then get to work!!