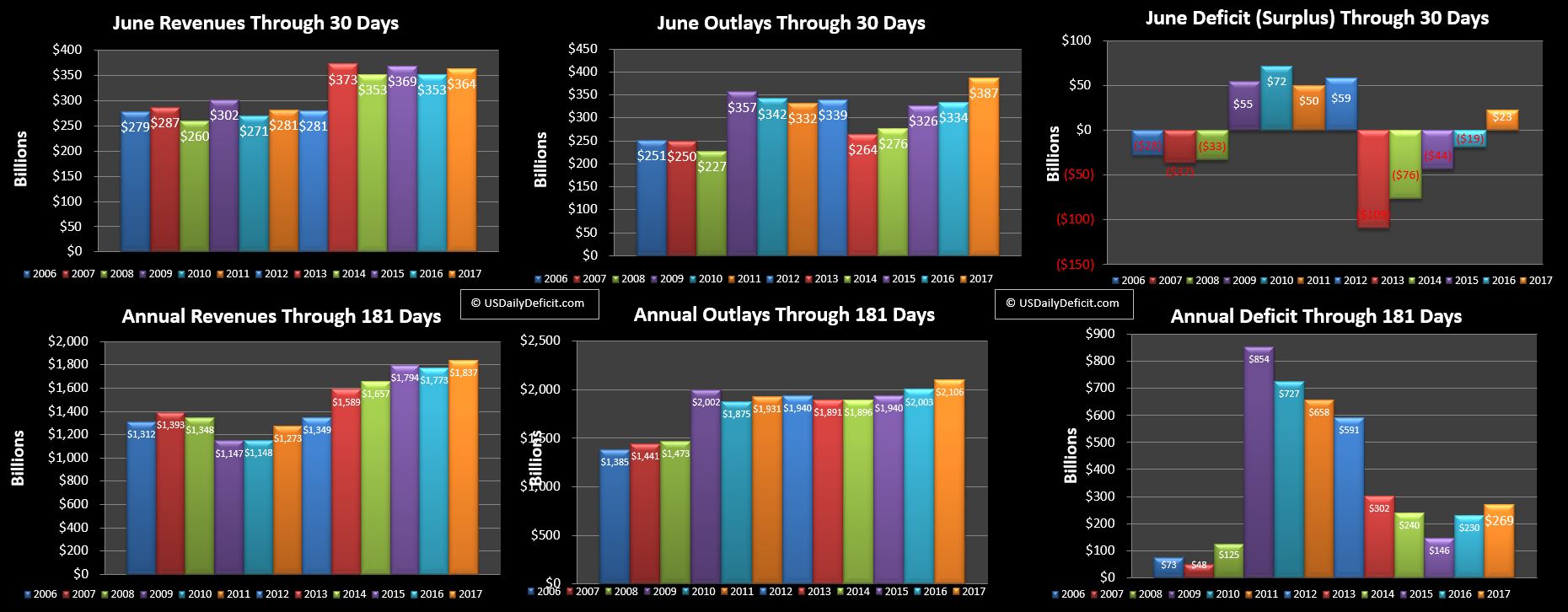

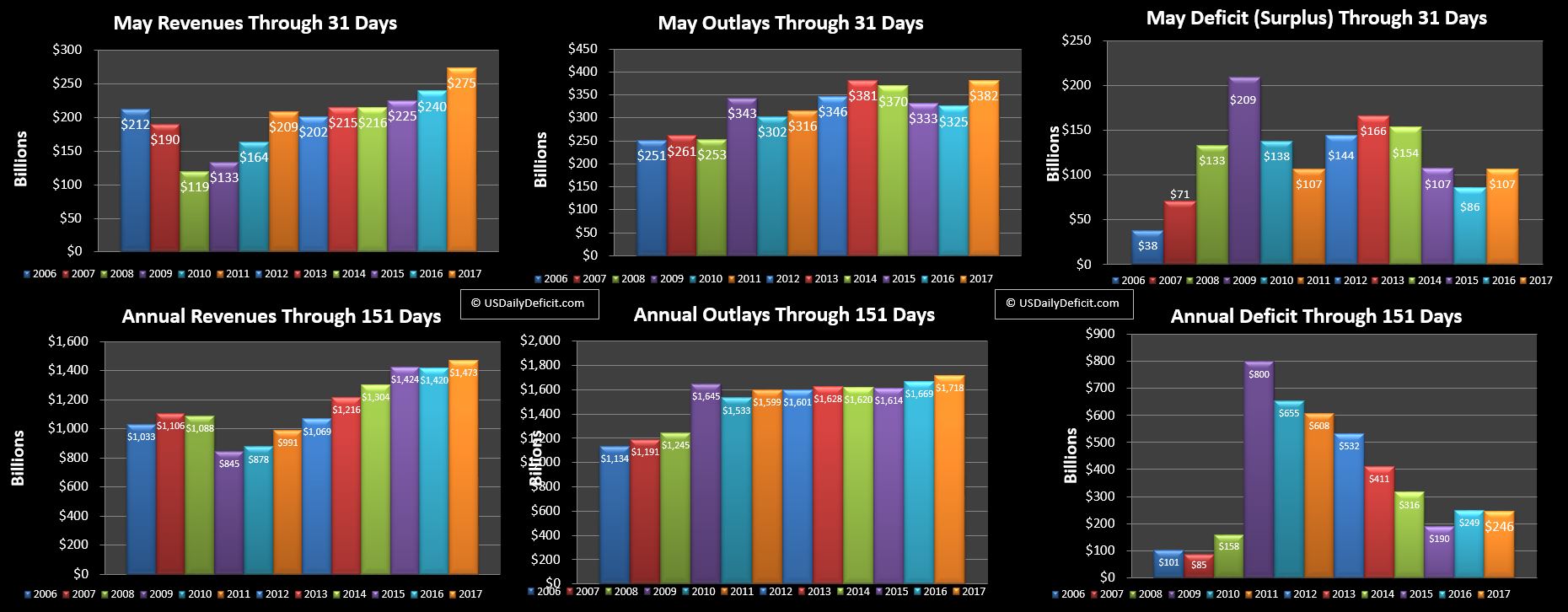

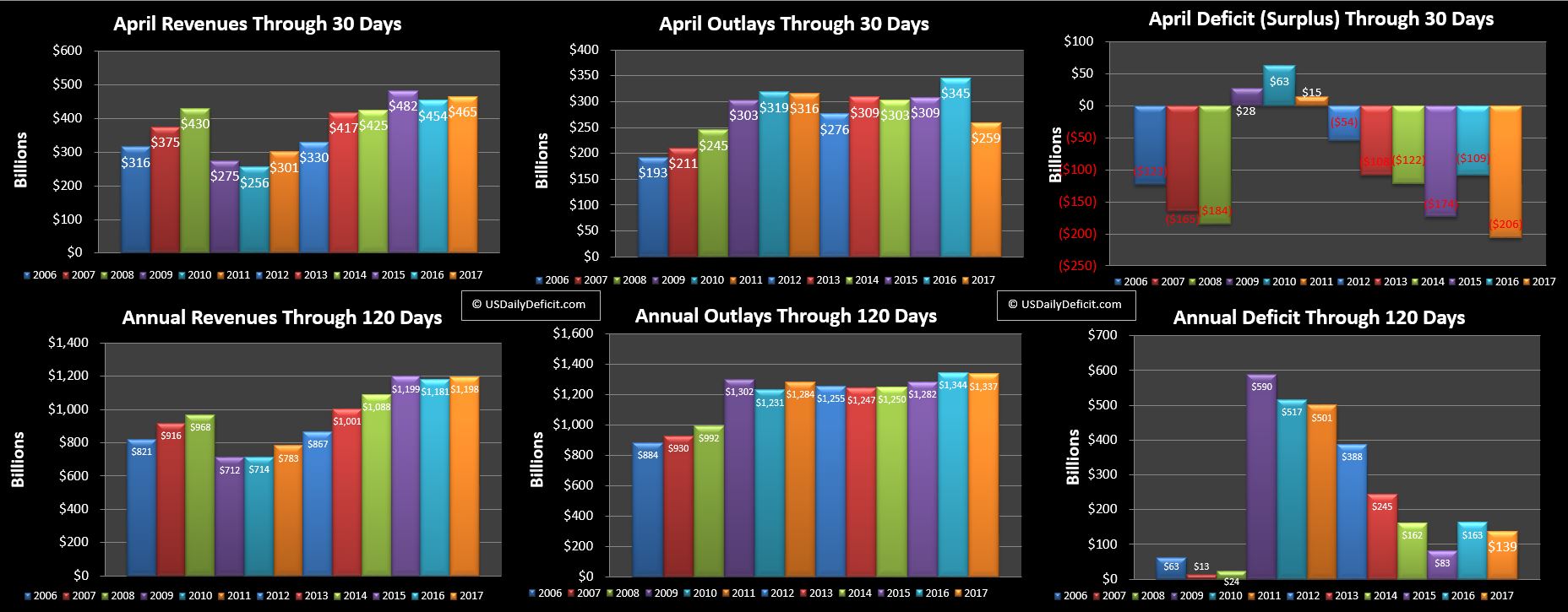

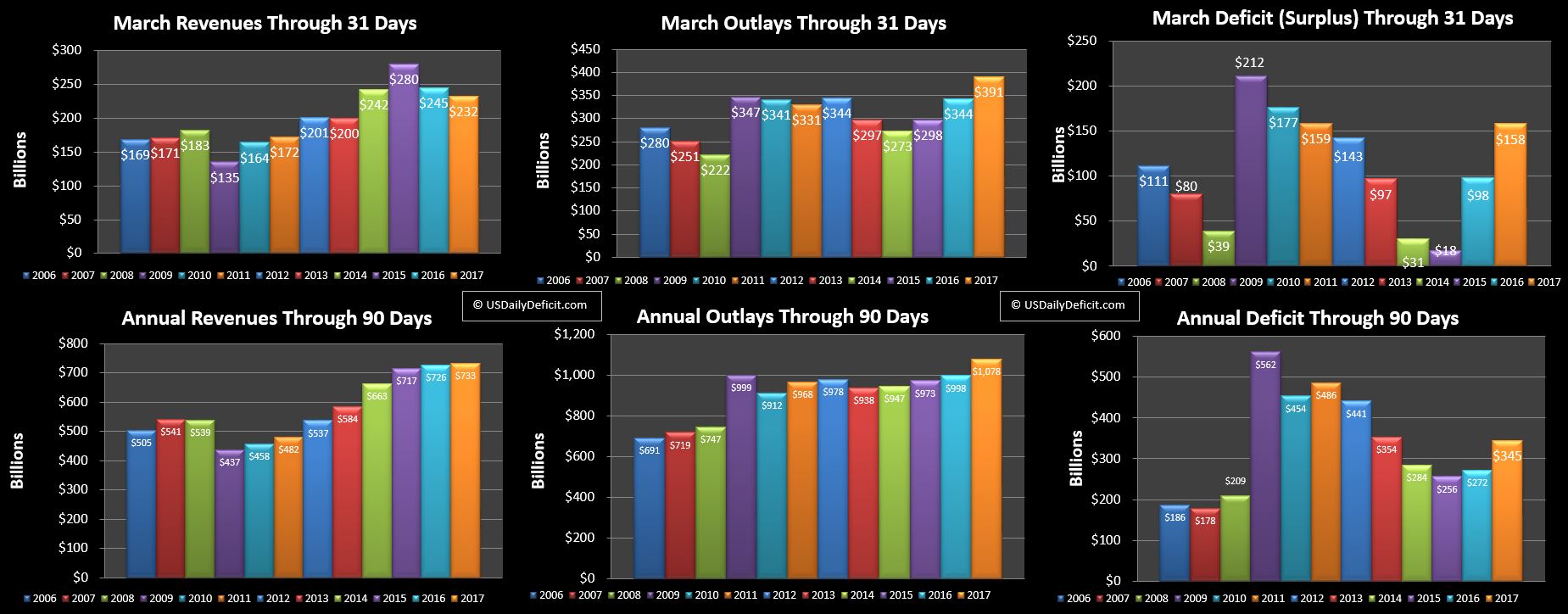

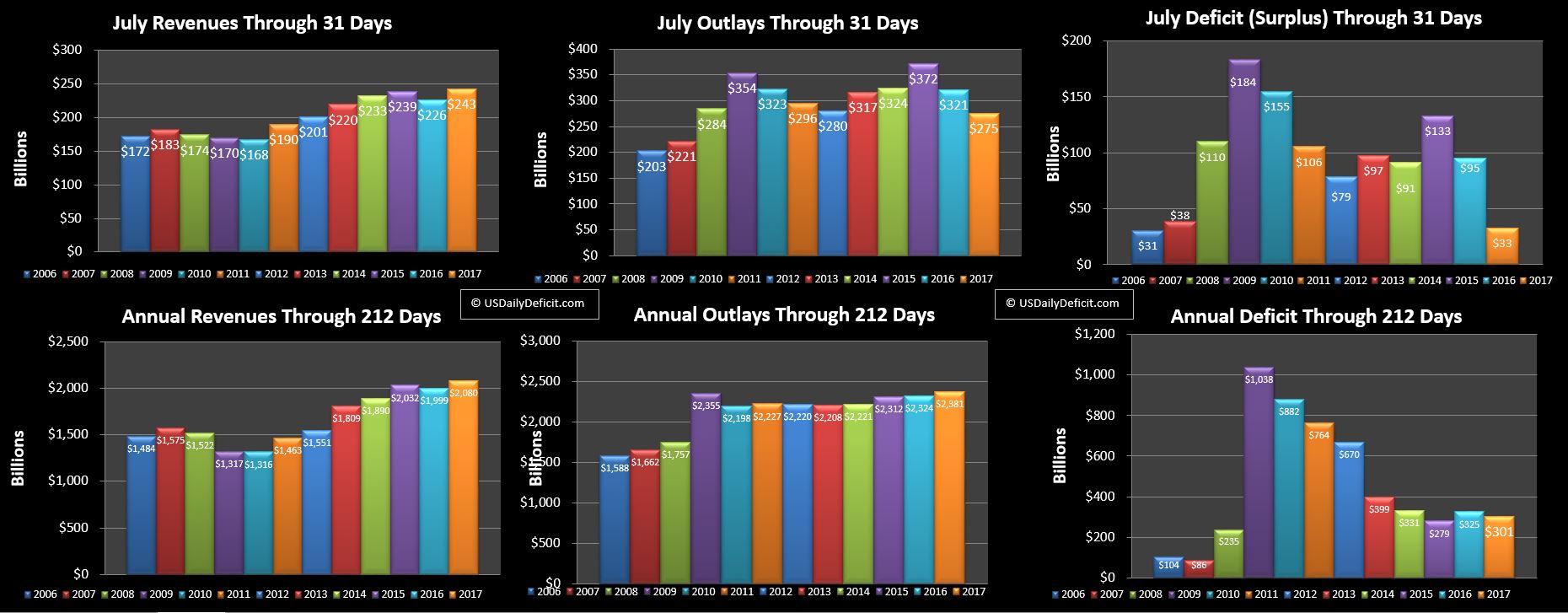

Not a bad looking month….Some of the revenue beat was timing, but the YTD is now at +4%. All of the outlay beat was timing, and the YTD oulays are up 2.5%. So far, through 7 months the revenue increase is just edging out the increase in expenses and as a result the deficit is down $24B….

Down is good, but it’s not a spectacular number….and since Treasury is now hiding hundreds of billions of debt via extraordinary measures(EM) to circumvent the debt limit…there’s a good chance some of this is illusory, but we won’t know for sure until the debt limit is increased, probably in the September-October time frame. Don’t get me wrong, it shouldn’t be a huge revision, but it could make +$24B disappear in the blink of an eye….or not, who knows 🙂

Looking forward…August will not be kind to Treasuries cash balance, currently at $189B, look for a ~$125B+ deficit, and a cash draw in that ballpark depending on how much EM they have left in the secret book of tricks.