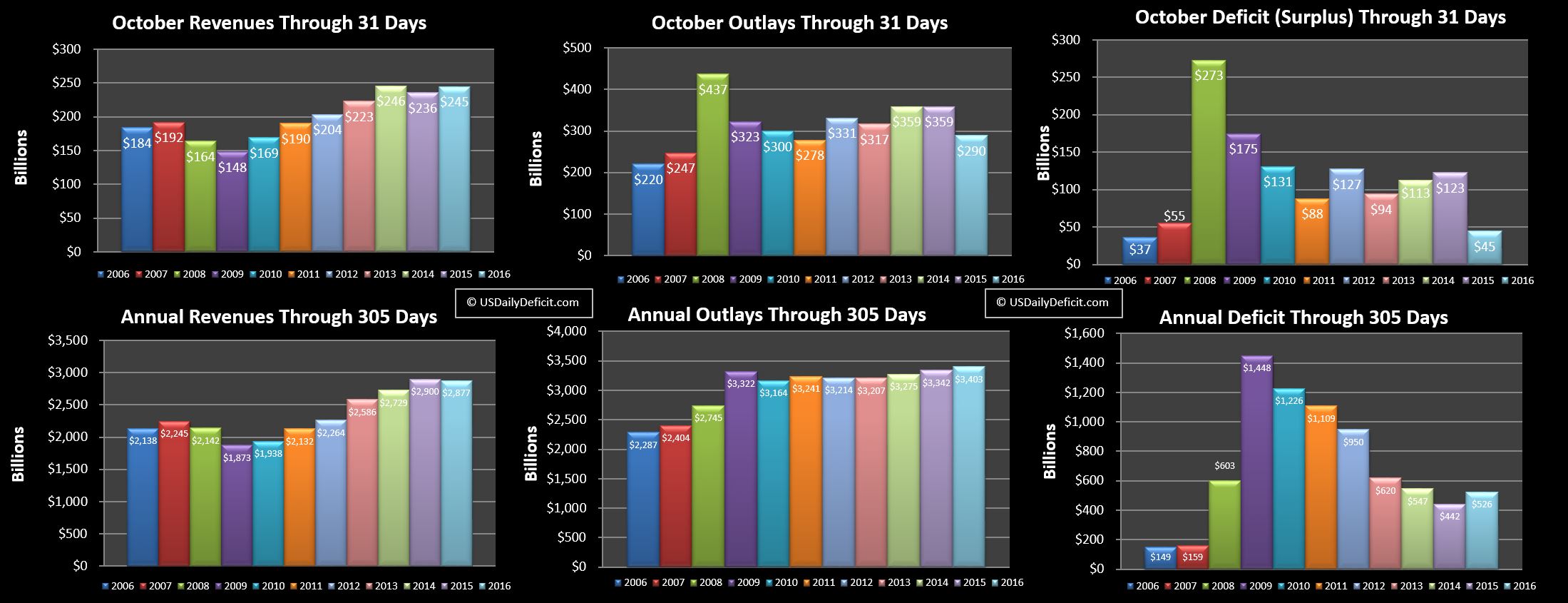

The US Cash Deficit for October 2016 came in at $45B for the month, bringing the year through 10 months to $526B.

Revenues:

Revenues were up 4% climbing $9B to $245B compared to last October’s $236B. That’s fairly impressive especially on the back of withheld taxes being up 8%, all on one less business day than last October. For the year, revenues are still down $23B, certainly within striking distance to top last year, but still almost certain to be a poor showing for the year even if we do manage to top last year, which is far from certain.

Outlays:

At first glance, outlays were down huge from $359B to $290B. It turns out that we have two timing events doubled up that account for the dip. First up, ~$45B of cost due this October 1, actually went out at the end of September due to the weekend timing, leaving this October’s number artificially low. Second, last October was artificially high due to the same reason, payments due November 1 were paid at the end of October, boosting last Octobers spend. At the end of the day, these timing issues net out, so a few days into November we are right back where we started, running about 3% over last year.

Deficit:

At $526B, we are running nearly $100B over last year and headed to end the year over $600B, ending 6 straight years of deficit improvement dating back to 2010.

Summary:

It is encouraging to see withheld taxes at +3.9% for the year, indicating that the employment gains we are seeing are translating into increased tax revenue. Offsetting that is taxes not withheld(-6%), corporate taxes(-12%), along with increased tax refunds, which I count as negative revenue. One can hope that next year payroll taxes continue to increase at this solid rate, and the other tax categories stabilize or even improve, leaving us in the +3% ballpark. In the meantime, it’s bad and getting worse, but not particularly quickly. As far as I can tell, neither Clinton or Trump has a legitimate plan to fix this problem, leading me to believe we could be back in the $1T per year ballpark much quicker than the current trend line indicates. Stay tuned… between the election, year end, tax season, and a March 2017 debt limit, tis the most interesting time of the year!!