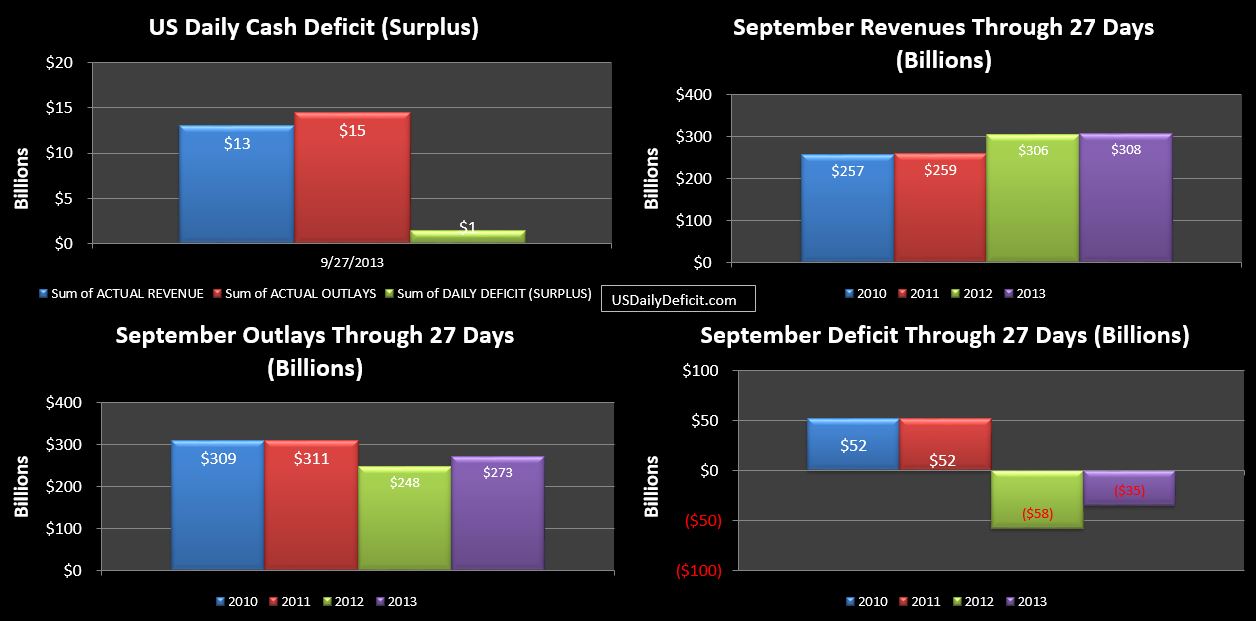

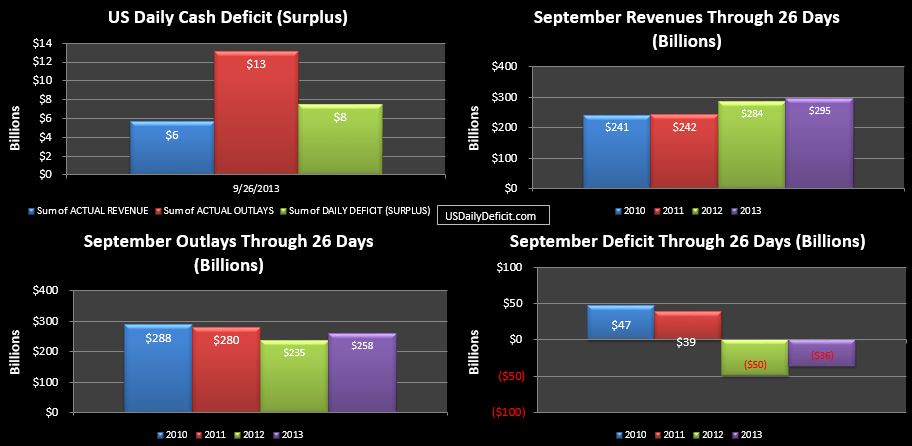

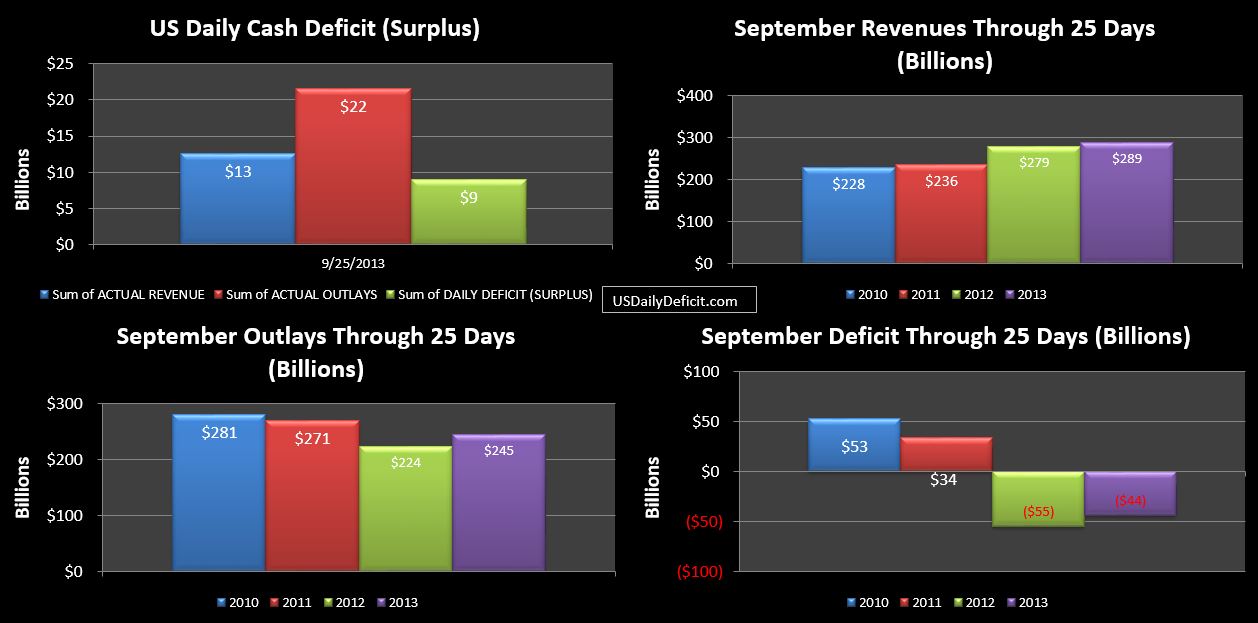

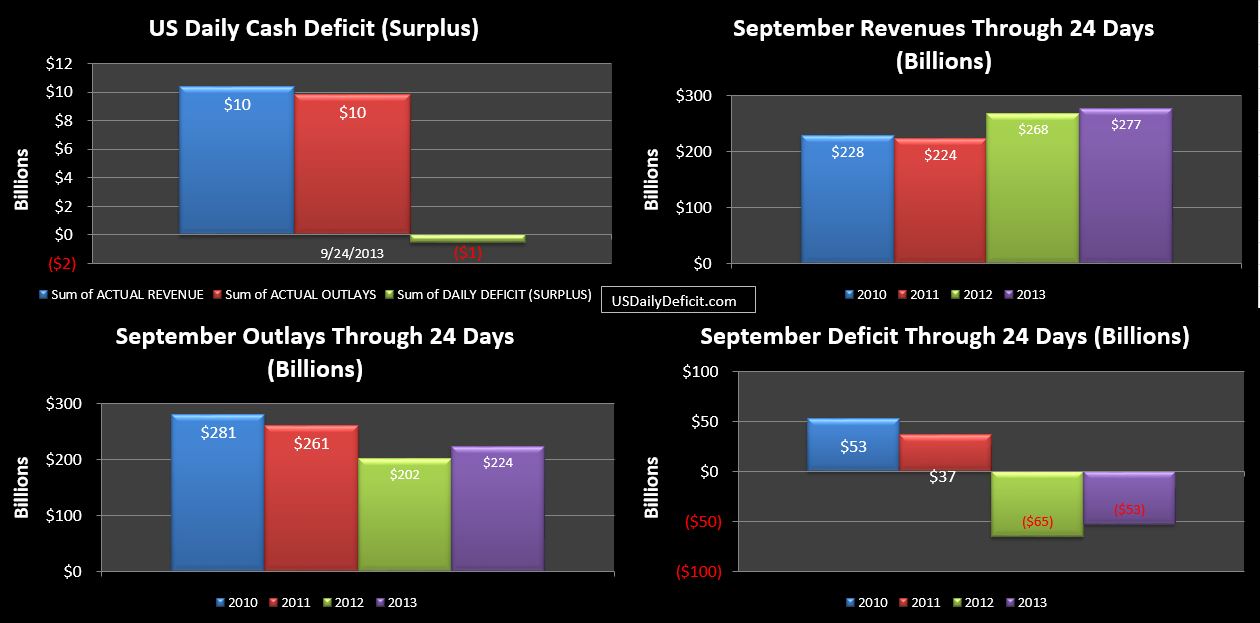

The September numbers were just released…. the total Social Security population grew 140k to 57.695M people, with the average recipient receiving $1,162 per month. Penciling that out yields a very large number, but that’s not really what I am interested in. I watch this series because I am looking for a material change in the rate of retirements….which is what we would expect some time soon as we get into the meat of the baby boomer retirements.

For some reference, in the late 90’s, we were adding about 300k people to Social Security programs(Old age and disability) per year. By 2006/2007, the rate had edged up to about 700k per year of additions before spiking to over 1.6M in 2009 as millions jumped onto Social Security/disability after losing jobs due to the recession. Since then, it had slowly been drifting down, with the latest annual rate being 1.248M additions per year. For the month, last September had 155k additions, 15k higher than this September so the slow drift downward is continuing, but we are still adding a lot of people each year.

I guess you could say it’s a good thing that the rate is coming down, but the truth is, we are still adding people at a phenomenal rate, and that rate will likely be heading back up before too long. For reference…while SS is adding an average of 104k people to it’s rolls each month…the total population is growing at about 187k per month, and jobs are being added at 184k per month over the last 12 months. On the cost side, we are seeing growth of about $62B per year due to growth in the population and the annual cost of living adjustment. So all else equal, to keep the budget deficit constant, we need either 62B of new revenue each year, or need to make $62B in cuts….each year in perpetuity, and that # will probably start accelerating up over the next 5 years. So it’s bad, and getting worse. Remember all the drama last year surrounding the $85B sequestration?

Finally, just a thought on retirement choices. For most, you have a choice to apply for social security from when you turn 62 all the way up until 70, but the longer you wait, the more money you get. I suspect that for those who can, they try and work as long as they can. However, during the “great recession” many in the 62+ age group who lost their jobs couldn’t find jobs, and therefore took social security earlier than they would have liked at a reduced rate. Now, the economy isn’t quite as terrible, so more seniors are working just a tad longer…delaying their retirement, but ultimately increasing their potential payout. So while that may be temporarily suppressing boomer retirements, in the long run, the higher payments could actually make the long term situation worse.

On the other hand….why worry about the long run. The odds of this turd staying afloat for another decade, much less 30+ years is slim to none. I suppose one of the reasons I do this is just to document the absurdity in real time. None of this is rocket science. Anybody with a spread sheet and the ability to do middle school level math should be able to sit down and see that none of this will end well….and yet, a (vast?)majority of politicians and citizens seem deluded enough to believe we can just keep kicking the can. Hint Hint….we can’t 🙁